What employers need to know about their UI rate

Between January and March each year, New York State employers receive their Unemployment Insurance (UI) Rate Notice from the NYS Department of Labor. These notices establish your unemployment tax rate for the calendar year — and they are retroactive to January 1.

If you haven’t looked closely at yours yet, now is the time.

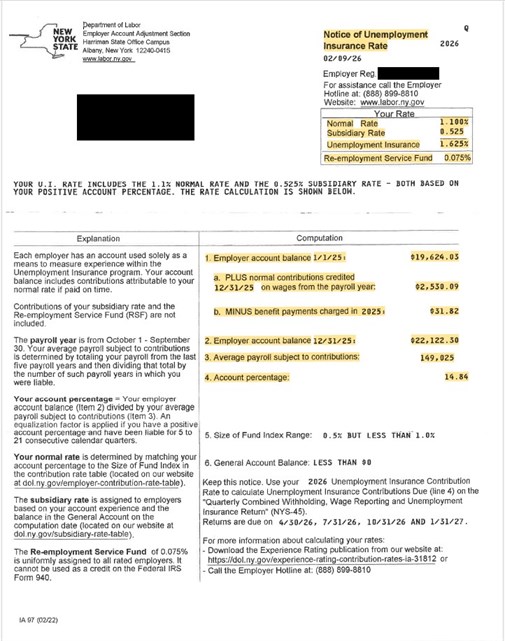

Below is a sample 2026 rate notice and an explanation of the key highlighted sections so you understand exactly what you’re looking at — and what it means for your business.

Understanding the Key Sections of Your 2026 Rate Notice

|

|

| |

Your Rate Breakdown (Upper Right Section)

This box shows the components that make up your total unemployment rate:

Normal Rate

This is your experience-based rate, determined by your account percentage and your claim history. In the sample shown, the normal rate is 1.100%.

Subsidiary Rate

This additional rate is assigned based on the balance of the state’s General Account. In the sample, it is 0.525%.

Unemployment Insurance Total Rate

This is the combined total of the Normal Rate and Subsidiary Rate. In the example: 1.625%.

Re-employment Service Fund (RSF)

Currently 0.075% for all rated employers. This is added to your total contribution but cannot be used as a federal credit.

Your unemployment cost is calculated by applying these percentages to wages subject to unemployment insurance.

How the State Calculates Your Rate

The Department of Labor calculates your unemployment rate using what is essentially a reserve account formula. Think of it like a checkbook.

Each employer has a reserve account that tracks activity over time. The calculation works like this:

Your quarterly tax payments throughout the year make up the “contributions paid” portion of this formula.

Using the sample notice:

The ending account balance is then divided by your average payroll subject to contributions. That result becomes your account percentage. That account percentage is matched against the state’s contribution rate table to determine your Normal Rate.

Average Payroll Subject to Contributions

This figure represents your average taxable payroll over the applicable calculation period.

Why Your Rate Changes

Your unemployment tax rate is directly affected by:

Unemployment tax is a controllable business expense.

An employee who is terminated for misconduct is generally ineligible to collect benefits. However, the employer must respond to the claim and provide documentation. If you do not respond, the benefits are typically charged to your account. Strong policies, consistent corrective discipline, and properly handled separations make a measurable difference over time.

For HR One Clients Utilizing Our Unemployment Insurance Administration Service

HR One reviews all assigned tax rates from the NYS Department of Labor. We evaluate whether a voluntary contribution would reduce your rate and generate net savings.

If a voluntary contribution is recommended, you will receive a direct email from our team outlining:

If you do not receive an email from us, it means:

You are already at the minimum rate, or a voluntary contribution would not generate meaningful savings.

These analyses are conducted annually.

For HR One Payroll Clients

As your payroll provider, our role is to ensure the correct unemployment tax amount is remitted with your quarterly filings.

If your rate decreased

You will receive a refund for over-collected amounts.

If your rate increased

We will impound the difference between what was previously collected and what is now owed so that your quarterly filings remain accurate.

If your rate stayed the same

No adjustment is required.

As you receive these notices from the state, please forward them to Sara Huck at shuck@peopletopayroll.com. We are making adjustments throughout the month, and employers should expect to see updates reflected by March 31. We will notify you of any refund or impound amount specific to your organization.

If you have questions, contact our customer service team at (315) 252-9150. Please keep in mind that these rate audits occur every year.

For All Employers

It is essential to understand your unemployment tax rate because it reflects your employment practices. Every claim filed and every week benefits are paid is a withdrawal from your reserve account.

If you would like assistance reviewing your rate notice, evaluating a voluntary contribution, or strengthening your unemployment risk management practices, our team is available to help.

Some nonprofit organizations participate in the unemployment insurance system under the direct reimbursement method rather than the tax-rated system described above. Instead of paying unemployment taxes based on an assigned rate, reimbursing employers repay the New York State Department of Labor for the actual cost of benefits paid to former employees. Because of this structure, nonprofit employers in the reimbursement program do not receive an annual unemployment rate notice, but claims filed by former employees still directly impact the organization’s costs.