Surcharges ending, benefits increasing

|

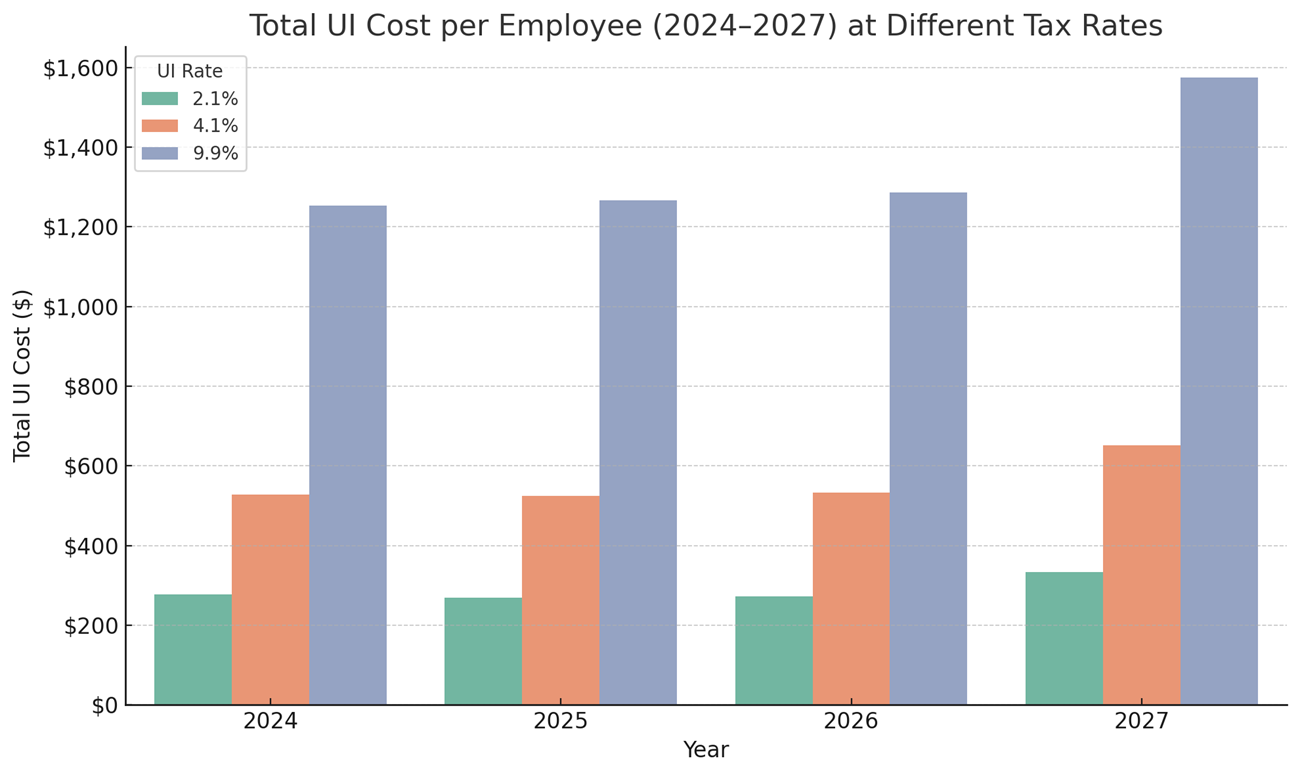

New York State’s FY2026 budget includes a comprehensive overhaul of the Unemployment Insurance (UI) system that delivers immediate cost relief for employers while also setting the stage for longer-term structural changes. The state is using $8 billion to eliminate pandemic-related UI debt, which will remove the Interest Assessment Surcharge (IAS) and lead to lower UI contribution rates for many employers beginning in 2026. At the same time, the budget increases the maximum weekly UI benefit for workers, raises the taxable wage base starting in 2026, and introduces an indexing system that will automatically adjust the wage base each year beginning in 2027. While these changes aim to stabilize the system, they will also gradually shift more of the funding burden onto employers in future years.

Short-Term Relief

To wipe out the pandemic-era debt owed to the federal government, Governor Hochul and state lawmakers have committed $8 billion in state reserves to pay off the UI Trust Fund’s remaining balance. This move brings immediate relief in two ways:

These changes offer a welcome break for small businesses that have seen elevated unemployment costs since 2021. That said, individual savings will still depend on each employer’s UI rate, which is tied to claims history and other factors.

What’s Changing and When

This indexing system is intended to strengthen the Trust Fund over time — but it also means employers will be paying UI tax on a steadily growing portion of each employee’s wages.

Long-Term Considerations

While the 2026 budget reduces UI costs in the short term, it also lays the foundation for more permanent changes, some of which may increase costs for employers in the years ahead.

Simply put, the state’s goal is to strengthen and better fund the UI system — but this will gradually place a greater share of the financial burden on employers.

What This Means for HR One Clients

|

|

|

(Click the image to enlarge) |

If your business has been burdened by UI taxes since the pandemic, this budget delivers meaningful short-term relief by doing away with the IAS and lowering rates. But it also marks the beginning of a shift: lower rates will be paired with higher taxable wages, and the rising benefit cap will make every claim more expensive.

Now is a good time to review your current UI rate and claim history. While unemployment costs remain manageable, there are steps employers should be taking to keep costs down, including:

Conclusion

This is a step toward stability, but not a return to pre-pandemic norms. Businesses should budget accordingly, anticipating a UI system that places increased expectations on employers to ensure long-term solvency and reliability for workers.

If you have questions about your UI rate and how you can take steps to reduce it, call Deb Hague, our Unemployment Manager at (315) 463-0004 ext. 303. Just have your most recent NYS UI rate notice or quarterly statement on hand, and she can walk you through what the numbers mean and what steps you can take to stay ahead of future cost increases.