Let HR One help with Affordable Care Act compliance and reporting

Ignoring the Affordable Care Act (ACA) or taking a “wait and see” attitude on complying with its provisions is no longer an option for employers. The law and the enforcement regulations that accompany it place a variety of responsibilities on employers and it can become overwhelming without assistance. HR One can help your organization to determine the portions of the ACA which your organization is subject to and what, if any, reporting requirements you may be subject to. For HR One payroll clients, our Payentry system has the tools that can actually assist you in completing the reporting and filing requirements. We will periodically be updating this page with the latest compliance information and the solutions available from HR One. If you have specific questions about the Affordable Care Act don't hesitate to contact us.

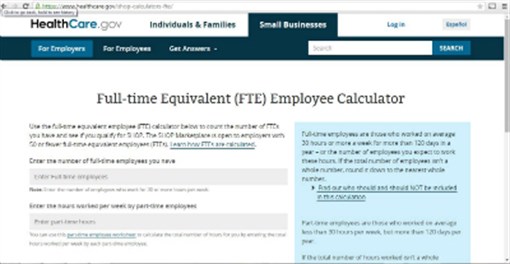

How can I determine which portions of the ACA my organization may be subject to? According to the IRS, the law contains benefits and responsibilities for employers. The size and structure of your workforce – small, large, or part of a group – helps determine what applies to you. For 2015 and after, employers with at least a certain number of employees (generally 50 full-time employees or a combination of full-time and part-time employees that is equivalent to 50 full-time employees) will be subject to the Employer Shared Responsibility (ESR) provisions of the Internal Revenue Code as Applicable Large Employers (ALEs). As defined by the statute, a full-time employee is an individual employed on average at least 30 hours of service per week or 130 hours per month. Additionally, regardless of the size of your organization, if you self-insure there are going to be filing and reporting requirements that apply. HR One and Payentry can help you make the determiniation as to whether or not your organization is an ALE. Not a Payentry customer? There is a calculator on the Healthcare.gov site that will help you make the determination:

Under the Affordable Care Act’s employer shared responsibility provisions, applicable large employers must either offer minimum essential coverage that is “affordable” and that provides “minimum value” to their full-time employees (and their dependents), or potentially make an employer shared responsibility payment to the IRS. The employer shared responsibility provisions are sometimes referred to as “the employer mandate” or “the pay or play" provisions. Coverage is considered affordable if the employee’s share of the annual premium for the lowest priced self-only plan is no greater than 9.56% of annual household income. Minimum value means that the plan will pay at least 60% of the total cost of medical services for a standard population.

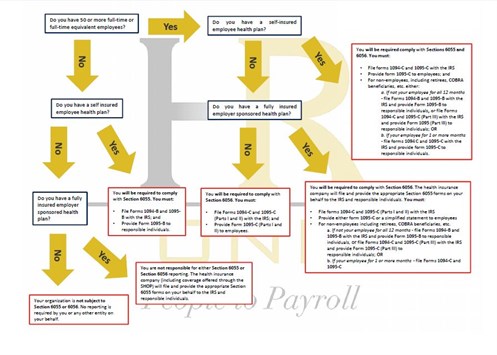

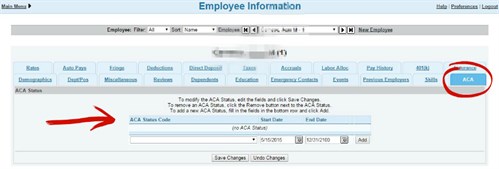

What are the reporting requirements for employers under the ACA? In order for the government to determine whether employers are meeting their obligations under the ESR provisions and whether individuals applying for subsidies through the individual markets aren't otherwise eligible for employer provided health insurance, there are certain reporting requirements that employers may need to comply with. A self-insured health plan means that your organization chooses to retain the costs and risks of health insurance internally, rather than transfer that risk to a third party, such as an insurance company such as Aetna or BlueCross BlueShield, which is the more traditional fully-insured plan used by most organizations. Section 6055 and 6056 of the Internal Revenue Code require insurance providers, including insurance carriers, plan sponsors of self-insured group health plan coverage, government agencies offering government sponsored coverage and applicable large employers to file information returns with the IRS and provide statements to their full-time employees about the health insurance coverage offered. For more on these requirements read this HR e-News from January 2015. How can HR One help with the reporting requirements? For HR One's payroll clients, the Payentry system has the tools to assist you in collecting and organizing the information you'll need for the reporting and will be able to file the reports for you in a timely manner. Within the system you'll have the ability to classify employees for purposes of the ACA as full-time or part-time, both as part of the new hire set-up as well as current employees under the individual employee information page under the "ACA" tab.

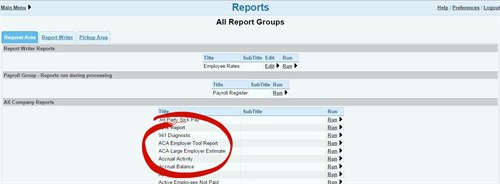

As you track employee status and hours throughout the year you'll also have the ability to generate reports that help organize the information you'll need for filing with the IRS and providing information to employees.

Current payroll clients of HR One can log-in to Payentry to verify that they are currently tracking this information and, if not, start to input the information for your employees. If you have questions about how to use the Payentry system to track this information and run the reports, contact us. What are some of the penalties I could be subject to?

Under the ESR provisions, if these employers do not offer affordable health coverage that provides a minimum level of coverage to their full-time employees and their dependents, the employer may be subject to a penalty, the ESR payment, if at least one of its full-time employees receives a premium tax credit for purchasing individual coverage on one of the new Affordable Insurance Exchanges, also called a Health Insurance Marketplace. An ALE member that fails to comply with the information reporting requirements may be subject to the general reporting penalty provisions under section 6721 (failure to file correct information returns) and section 6722 (failure to furnish correct payee statement).

|